Outlook for the “Main Street” M&A Market — Q4 2025

The Outlook: Market Steadies as Optimism Builds for Early 2026

DealStream has conducted its fourth quarter 2025 Market Survey, collecting responses from 519 active participants in the business-for-sale marketplace. As one of the world’s largest online platforms connecting buyers, sellers, and intermediaries, DealStream offers a real-time view of the dynamics shaping small-business transactions.

The Q4 results reveal a marketplace that remains active and resilient. Compared to Q3, confidence in deal volume has improved, buyer sentiment has strengthened modestly, and expectations for interest rate declines may fuel cautious optimism heading into 2026.

Defining the “Main Street” M&A Market

The “Main Street” M&A market represents the low end of the mergers and acquisitions spectrum, where businesses are typically valued at $5 million or less. This highly active segment — driven largely by independent owners and small operators — includes businesses like gas stations, restaurants, convenience stores, and local service providers. Unlike middle-market or large-cap transactions, “Main Street” deals are usually facilitated by business brokers, real estate brokers, and small intermediaries who specialize in connecting individual buyers and sellers.

DealStream is uniquely positioned to survey and analyze this market. With thousands of members using our platform to buy, sell, and broker deals, we have a direct lens into the sentiment among the people shaping this space every day.

Key Findings at a Glance

Here’s a detailed look at who took the survey and what they told us.

Survey Respondents: Demographics

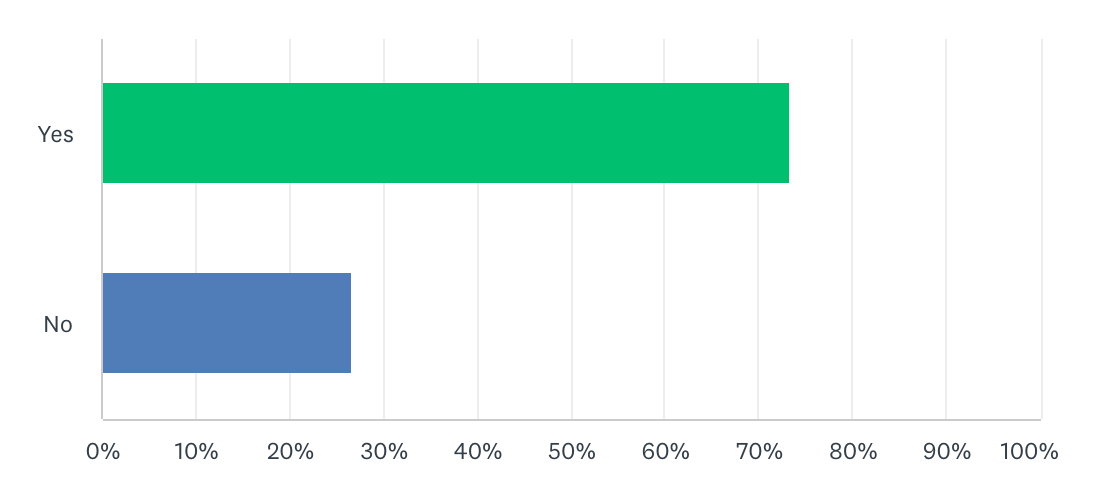

Q: Are you currently looking to buy a business?

Survey Results

Yes: 73% · No: 27%

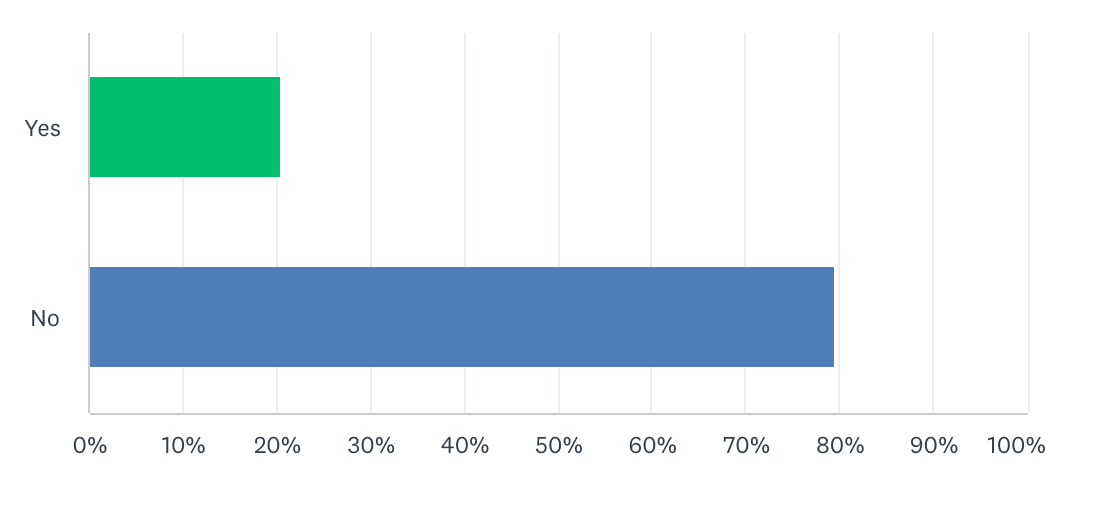

Q: Are you currently looking to sell a business?

Survey Results

Yes: 20% · No: 80%

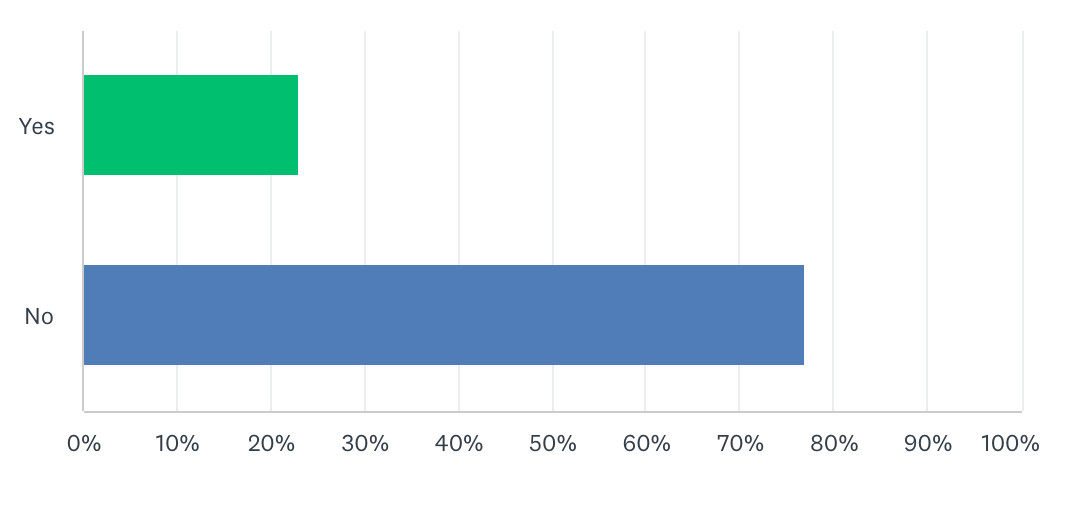

Q: Are you an intermediary (business broker, real estate broker, or investment banker)?

Survey Results

Yes: 23% · No: 77%

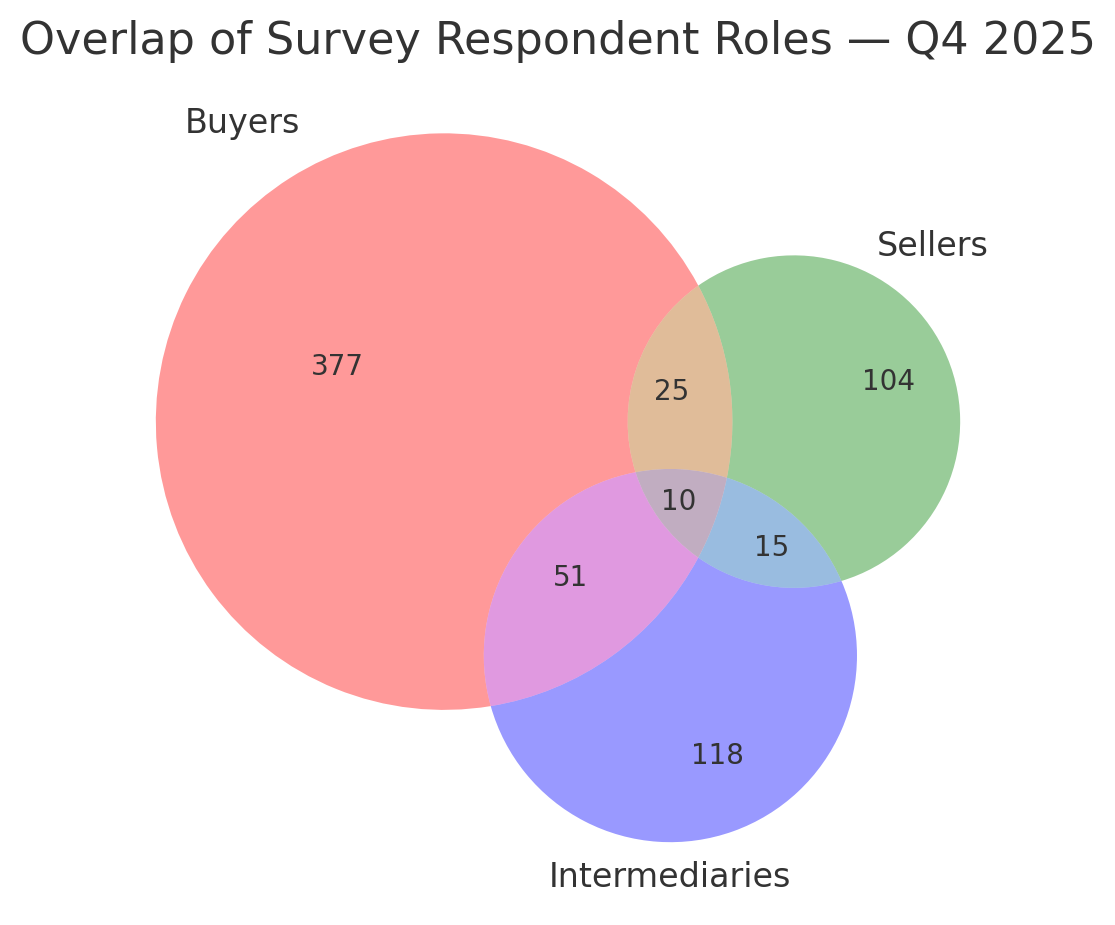

Here’s a closer look at how the survey respondent’s roles overlap:

Respondent demographics closely align with Q3 results, dominated by active buyers and a growing segment of intermediaries. Over 60 individuals reported serving in both capacities, illustrating the multifaceted roles common among professionals in this market.

Survey Results

Now that we’ve covered who participated in the survey, let’s dive into what they had to say. The next sections break down how buyers, sellers, and intermediaries view today’s market — from the economy and pricing expectations to deal volume and financing outlook.

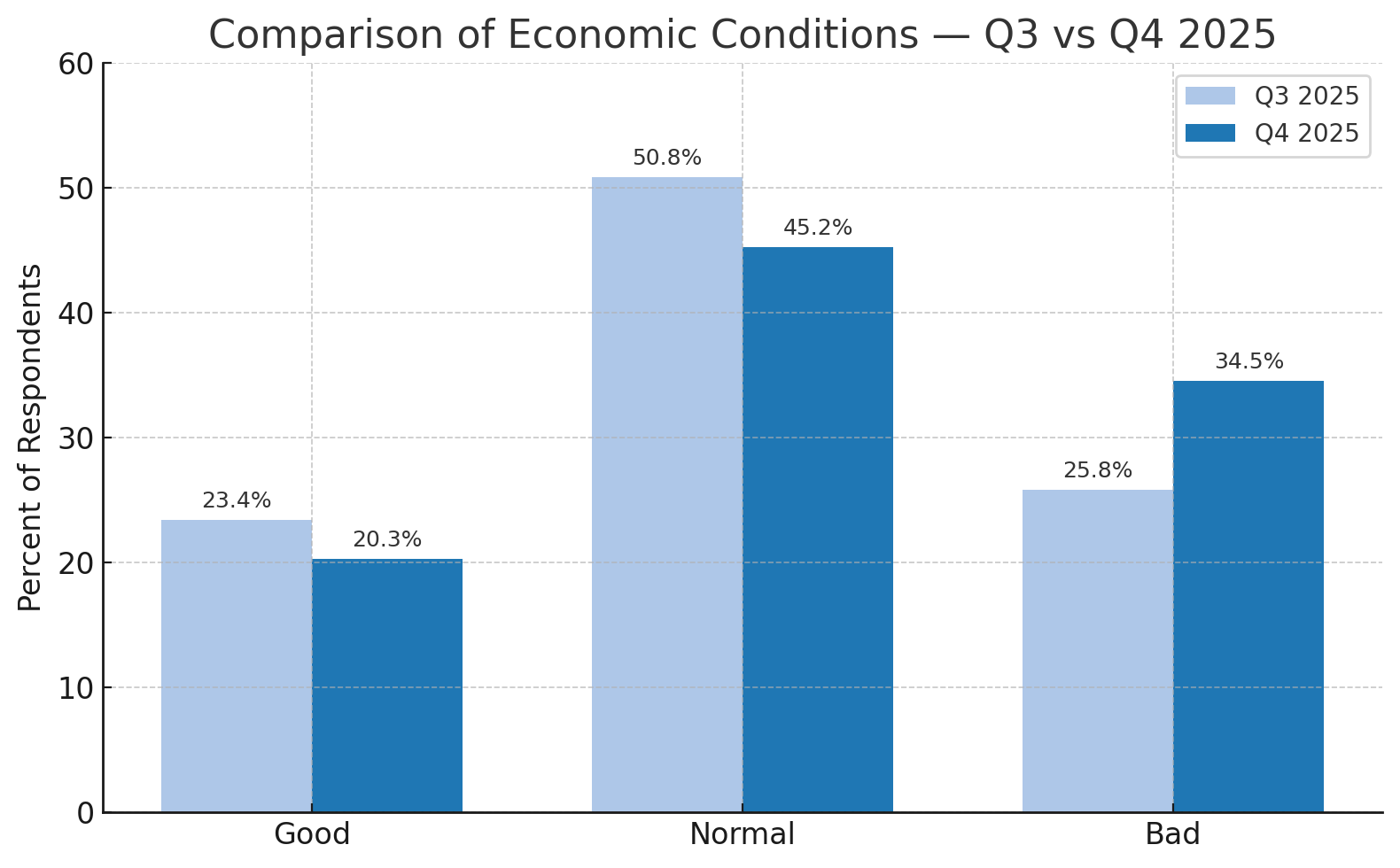

Economic Conditions: Signs of Strain but Continued Stability

Q: How do you rate current conditions in the overall economy?

Confidence Slips, but Stability Holds

Sentiment toward the overall economy softened compared to Q3. The share viewing conditions as “bad” rose nearly 9 points, while “normal” declined by about 6 points. Despite this shift, nearly half of respondents still describe the economy as “normal.”

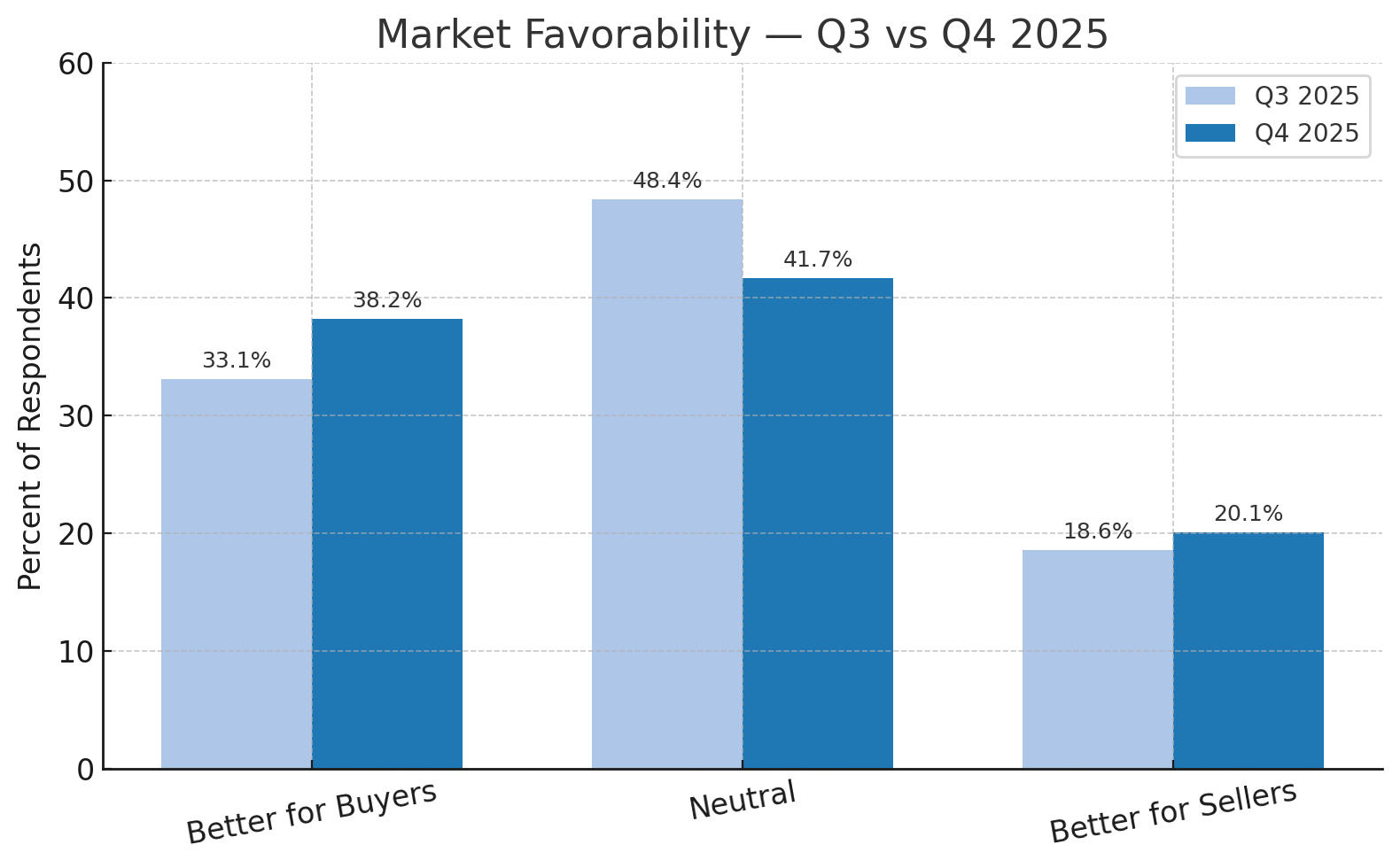

Buyers vs. Sellers: Advantage Still Tilts Toward Buyers

Q: Do you think the current market is more favorable for people looking to buy businesses or sell businesses?

Buyers Tighten Their Grip

The buyer advantage has strengthened modestly since Q3, while neutral sentiment has dropped. This suggests that while the market remains relatively balanced, respondents increasingly recognize a tilt toward buyers.

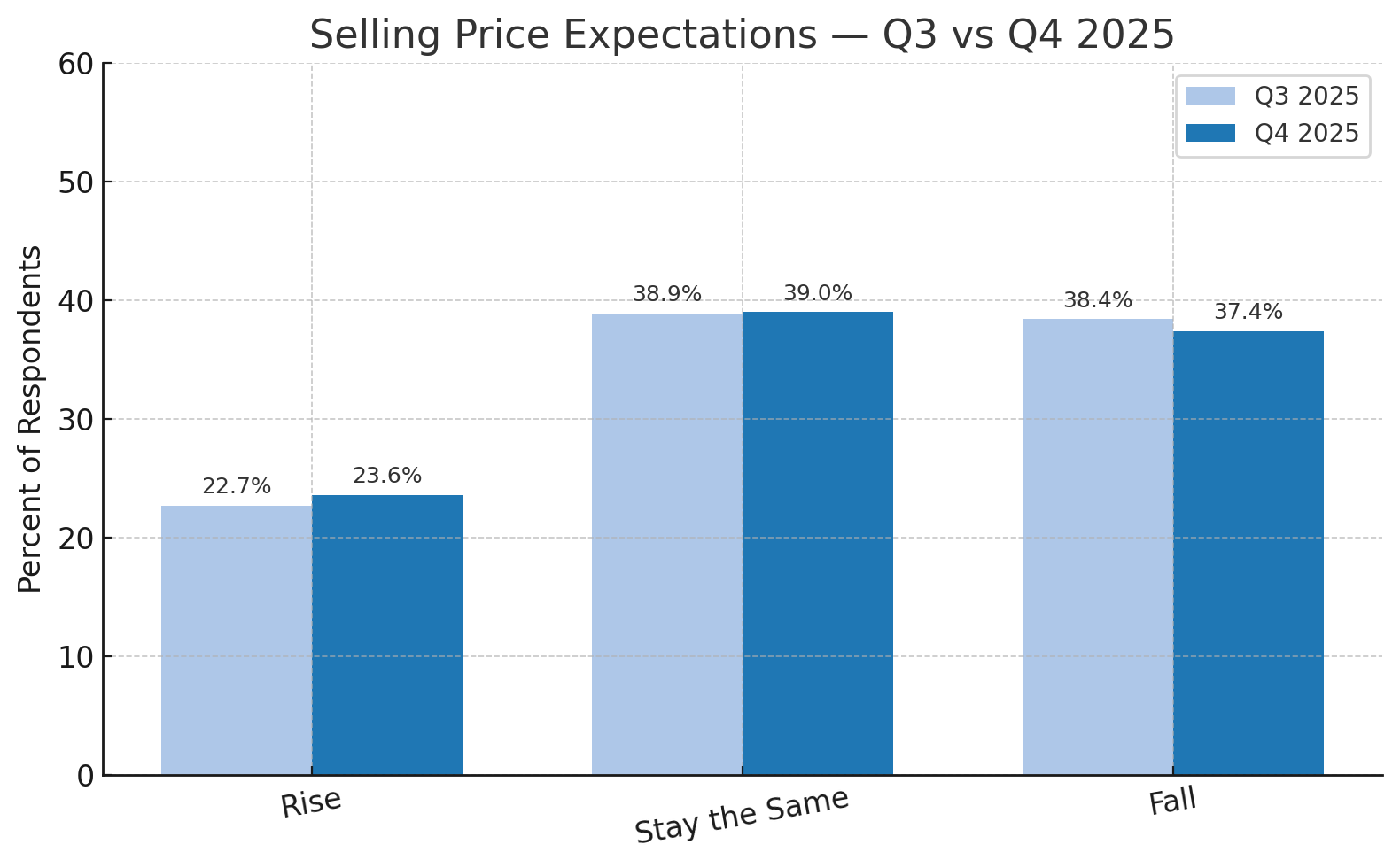

Price Expectations: Stability Persists

Q: Do you expect the selling prices of businesses to rise or fall over the next 6 months?

Valuations Level Off

Expectations for business valuations remain nearly identical to Q3. Roughly four in ten respondents expect prices to hold steady, and a slightly smaller share anticipate declines. The results suggest that price stability continues to define the “Main Street” market.

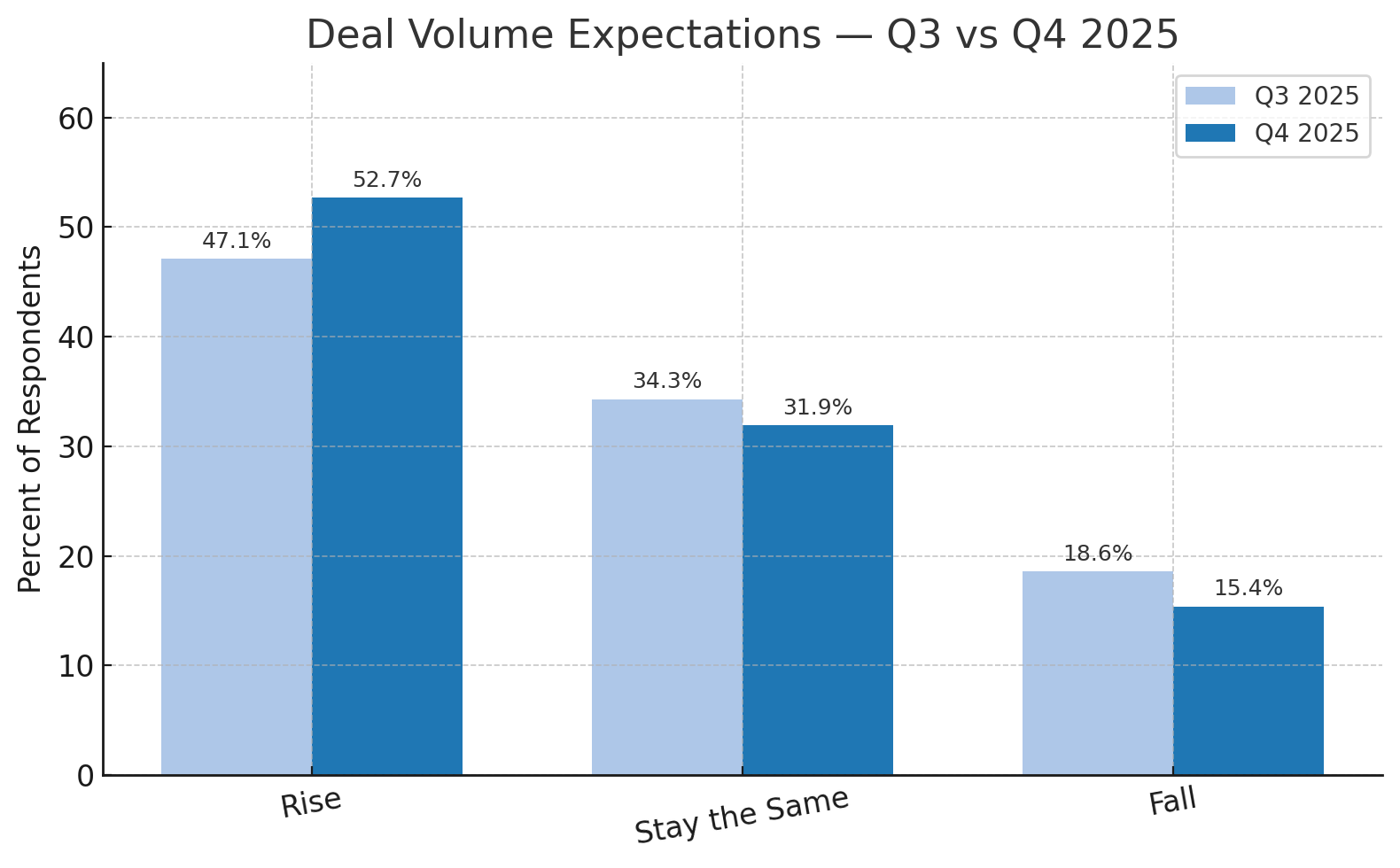

Transaction Volume: Confidence Builds for a Busier 2026

Q: Do you expect the number of businesses sold to rise or fall over the next 6 months?

Deals on the Rise

Optimism about transaction volume continues to grow. More than half of respondents expect an increase in business sales — up nearly 6 points from Q3 — while those expecting declines fell by over 3 points.

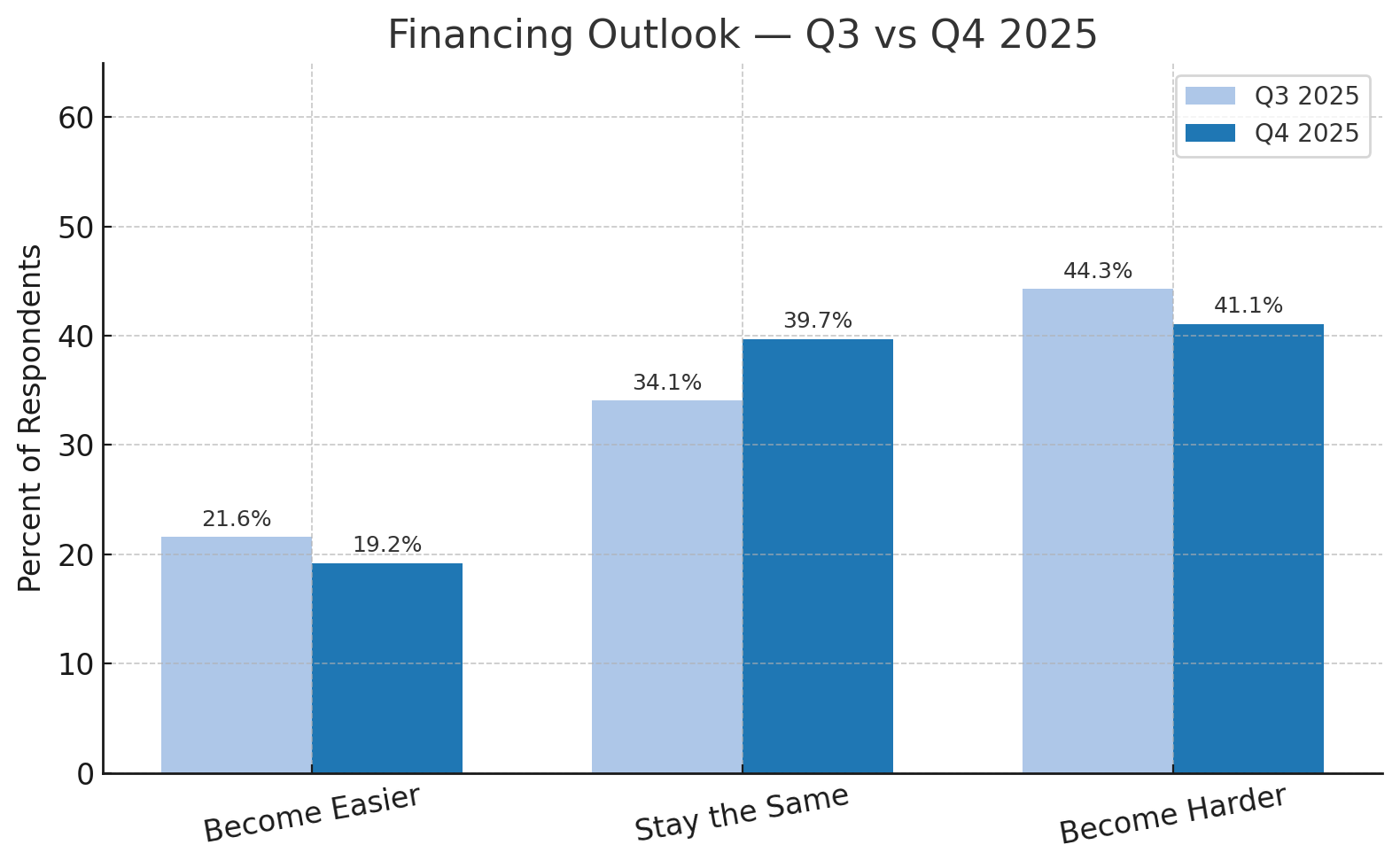

Financing Remains the Wildcard

Q: Do you expect it to become harder or easier for buyers to obtain financing over the next 6 months?

Credit Conditions Stabilize

Financing remains a headwind, but sentiment has improved modestly since Q3. Fewer respondents expect conditions to worsen, and more anticipate no change — a sign that fears of escalating borrowing costs may be easing.

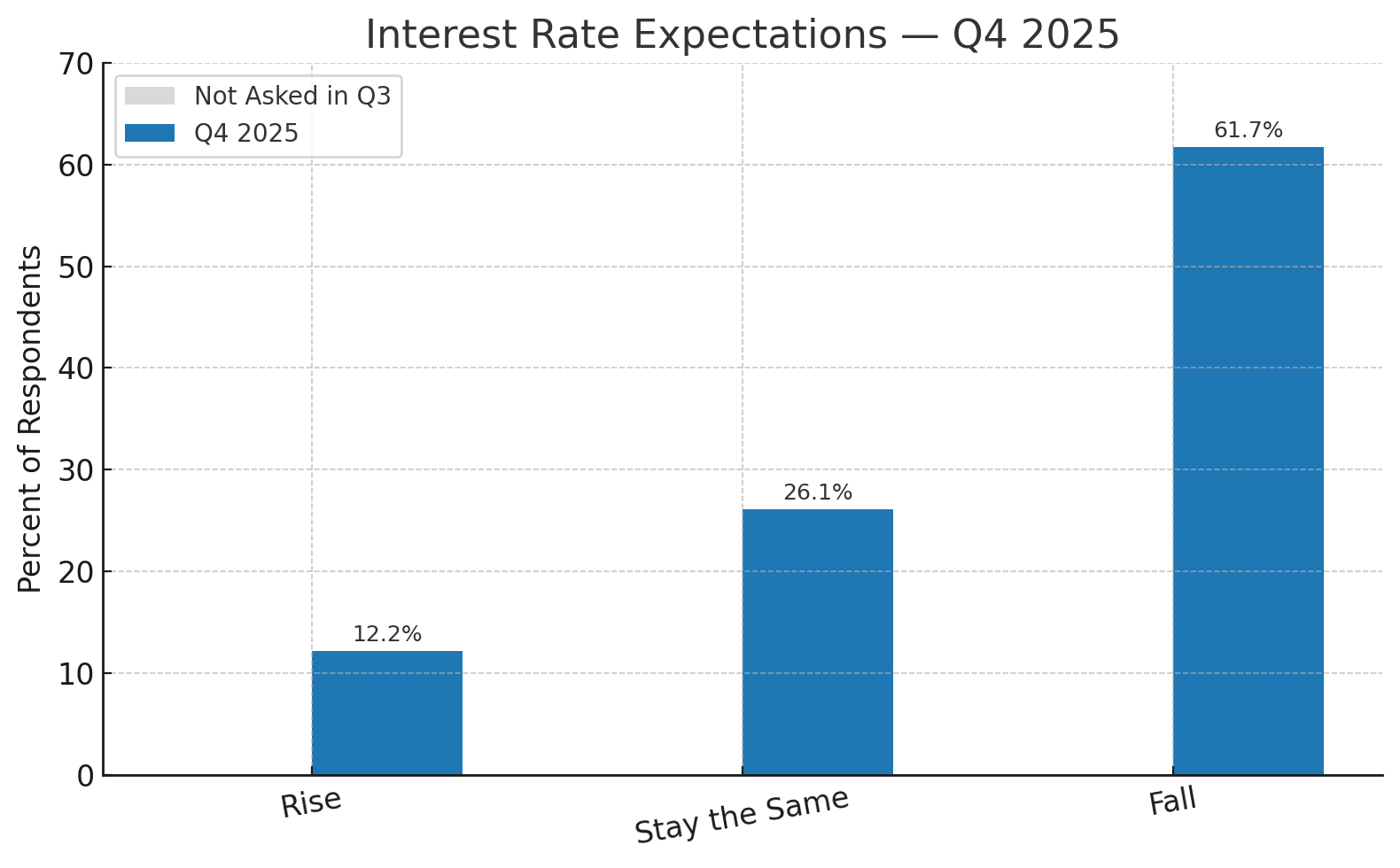

Interest Rates: Signs of Easing Ahead (New Question)

Q: Do you expect interest rates to rise or fall over the next 6 months?

Expected Rate Cuts on the Horizon

For the first time, respondents were asked about interest rate expectations. Nearly two-thirds expect rates to decline in early 2026 — a clear signal of confidence that monetary policy may turn more supportive.

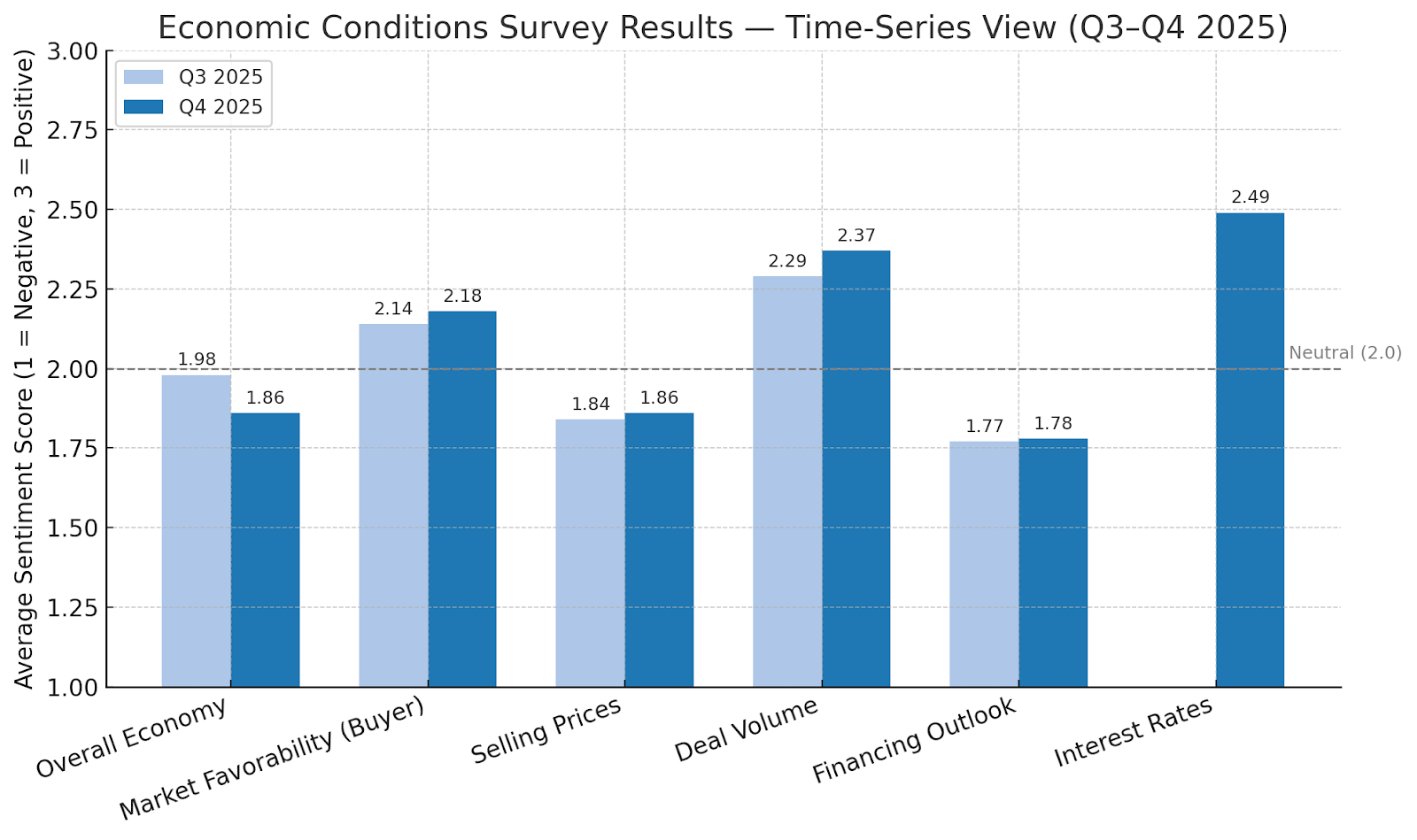

Economic Conditions: Time-Series Analysis

Next we summarized DealStream’s key market sentiment indicators using an average sentiment score, which converts respondents’ answers into a simple numeric scale (1 = negative, 2 = neutral, 3 = positive). Each score represents a weighted average of responses for that question, showing how overall confidence or concern shifted between Q3 and Q4 2025. Here’s what we found out:

Across all key indicators, sentiment in Q4 2025 remained largely consistent with Q3, signaling a stable but watchful market environment. Confidence in the overall economy softened slightly (average score 1.98 → 1.86), as more respondents rated current conditions as “bad.” However, several forward-looking measures saw some modest strengthening. Market favorability edged upward (2.14 → 2.18), reinforcing the view that buyers continue to hold the advantage. Deal volume expectations climbed (2.29 → 2.37), reflecting sustained confidence in near-term transaction activity.

At the same time, price expectations and financing outlooks showed little movement, suggesting that market participants are adapting to prevailing credit conditions rather than expecting dramatic shifts. The newly introduced interest rate expectations question revealed broad optimism, with an average sentiment score of 2.49, indicating that most respondents anticipate rates will decline in the coming months.

Overall, the data portrays a market that is steady, resilient, and cautiously optimistic as participants adjust to a high-rate environment and prepare for a potentially more favorable deal landscape in 2026.

Deeper Dive: Cross-Tab Analysis

Beyond the topline numbers, the Q4 2025 survey reveals important role-based differences that shape the dynamics of the “Main Street” M&A market. Buyers, sellers, and intermediaries each bring distinct perspectives influenced by their goals, exposure to financing constraints, and position in the transaction process.

By comparing responses across roles, we can see where sentiment aligns — and where it diverges — offering a clearer picture of who sees opportunity, who remains cautious, and why.

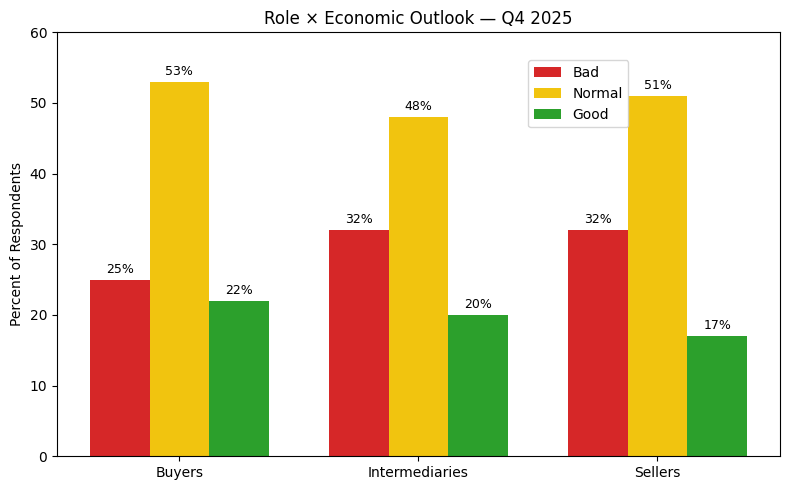

1. Role × Economic Outlook

Intermediaries Turn More Cautious

Buyers continue to report the strongest economic confidence, with 53% describing conditions as normal and 22% as good. Sellers and intermediaries are more cautious, each with roughly 32% rating the economy as bad. Compared to Q3, negative sentiment increased across all groups. While optimism has cooled slightly since Q3, the overall view remains steady — most respondents still see the economy as neither booming nor collapsing. Intermediaries in particular are balancing optimism among clients.

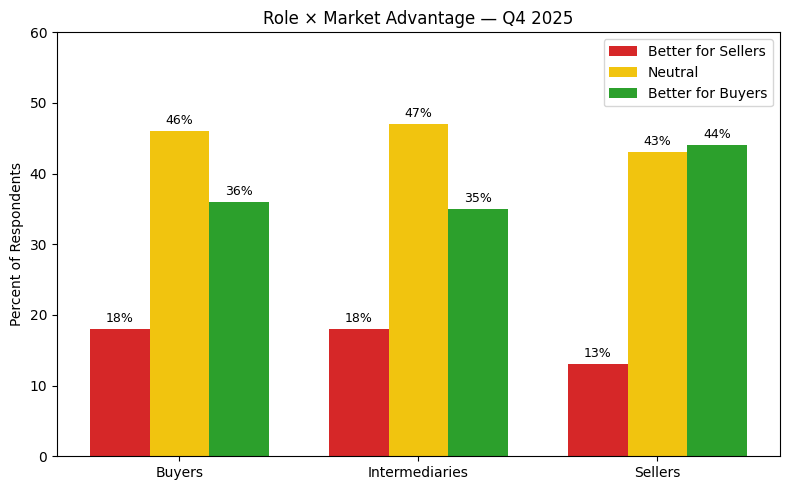

2. Role × Market Advantage

We next examined how respondents perceive leverage in today’s market. Each group’s view of who holds the advantage — buyers or sellers — reflects their proximity to ongoing negotiations.

Buyers Still Hold the Advantage

Across all roles, the consensus remains that buyers hold the upper hand. Roughly one-third of buyers and intermediaries share that view, while 44% of sellers also acknowledge a buyer-favored market. Neutral sentiment declined slightly from Q3. This quarter reinforces the view that the market favors buyers. Sellers appear realistic about current dynamics, while intermediaries continue to note relatively balanced conditions but with limited pricing power for sellers.

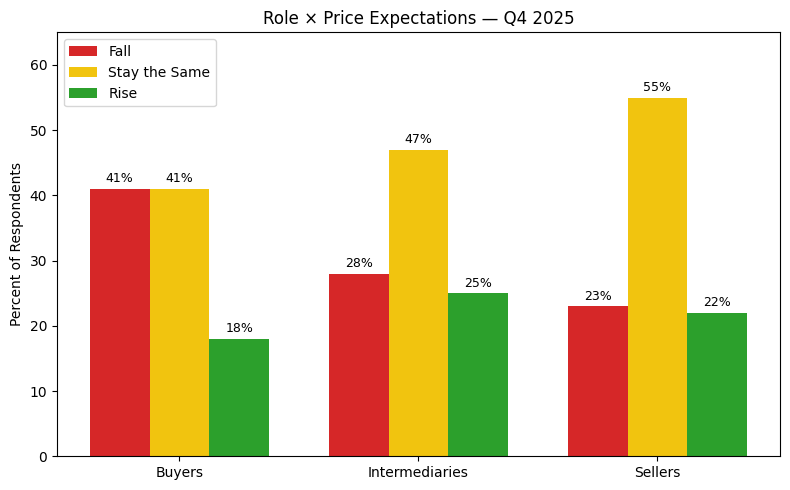

3. Role × Price Expectations

To understand how different roles view business valuations in the months ahead, we compared responses on expected price direction. Each role’s outlook reveals its exposure to pricing pressure.

Sellers Continue to Temper Their Price Outlook

Buyers anticipate continued price compression, with 41% expecting prices to fall. Sellers, by contrast, are the most stable, with 55% expecting prices to stay the same. Intermediaries fall between — 25% anticipate rising prices, 47% expect stability, and 28% foresee declines. Expectations remain consistent with Q3. Most respondents continue to predict flat to slightly lower prices.

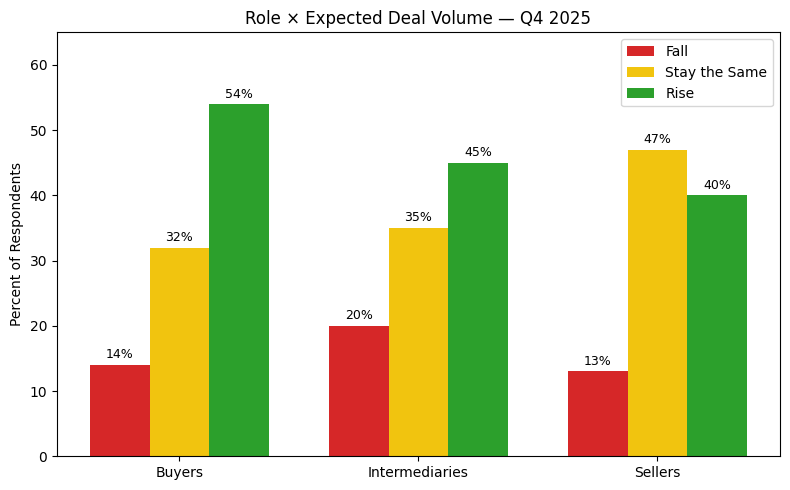

4. Role × Expected Deal Volume

To gauge expectations for transaction activity, we analyzed deal volume outlooks by role. This breakdown helps reveal which groups anticipate the most movement in the marketplace.

Optimism Builds Across the Board

Buyers are again the most optimistic, with 54% expecting an increase in deals. Intermediaries follow closely at 45%, while sellers are more conservative — 47% expect steady activity and only 40% foresee growth. Deal-flow optimism has improved since Q3. Buyers’ confidence suggests continued pursuit of opportunities even amid macro uncertainty.

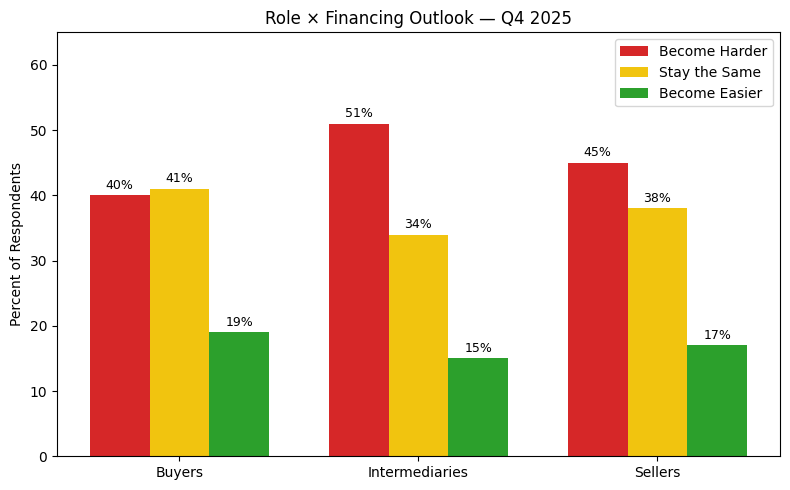

5. Role × Financing Outlook

Financing remains a critical factor shaping the business-for-sale market. Responses by role show how each group anticipates credit conditions evolving in the near term.

Credit Conditions Level Off

Intermediaries remain most concerned, with 51% expecting financing to become harder, compared to 45% of sellers and 40% of buyers. Encouragingly, more respondents in all groups expect conditions to stay the same rather than worsen — a shift of roughly 5 points from Q3. While credit access is still viewed as a headwind, sentiment has stabilized.

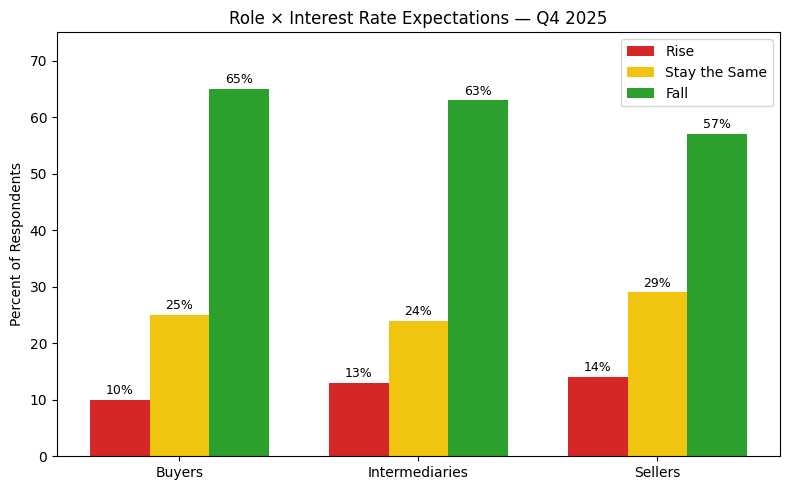

6. Role × Interest Rate Expectations (New in Q4)

This quarter introduced a new question on interest-rate expectations — a crucial factor shaping confidence in both pricing and deal volume.

Rate Relief on the Horizon

Across all roles, the majority anticipate rates will fall in the next six months: 65% of buyers, 63% of intermediaries, and 57% of sellers share this view. Only about one in ten buyers and one in seven sellers foresee further rate increases. Expectations of lower rates are reinforcing optimism for 2026, with most respondents predicting easing monetary policy.

Bottom Line

The Q4 2025 survey paints a picture of a resilient yet watchful “Main Street” M&A market. While concerns about the broader economy have grown modestly since Q3, optimism around deal activity remains intact. Pricing expectations are steady, buyer confidence is firm, and the prospect of lower interest rates in early 2026 is adding a note of cautious optimism across the board.

Consensus Findings

- Current economy is normal to soft

- Market balance continues to favor buyers

- Business prices are expected to remain stable or slightly lower

- Deal volume is expected to rise over the next six months

- Financing remains tight but is stabilizing

- Interest rates are widely expected to decline in early 2026

What This Means for Buyers and Sellers

Based on Q4 results, market sentiment remains constructive and continues to send a green light for both buyers and sellers. Buyers are seeing more opportunities as pricing levels out, while sellers are adjusting expectations and preparing for renewed activity in the year ahead. With credit conditions showing early signs of stabilization and expectations of lower borrowing costs, the environment may soon tilt toward more favorable deal-making dynamics.

Whether you’re preparing to buy, sell, or broker your next transaction, now is the time to plan strategically. Update your DealStream profile, refresh your acquisition or exit strategy, and stay ready to act when opportunity knocks. The next wave of Main Street deals is already building momentum — make sure you’re positioned to catch it.

Additional Resources

To help buyers and sellers prepare for successful transactions and beyond, DealStream has introduced a new series of Industry Guides.

These guides provide in-depth insights into valuations, market trends, and deal structures across key Main Street sectors — including restaurants, retail, healthcare, professional services, and many more.

Whether you’re exploring your first acquisition, running your dream business or planning your exit, these resources offer practical guidance for navigating today’s market with confidence.

We’d Love Your Feedback

DealStream values your insights and welcomes your thoughts on these findings.

To share feedback or ask questions, email us at submissions@dealstream.com.

Want to receive future survey results and market insights? Ask to be added to our mailing list when you reach out.

Your feedback helps us continue providing valuable perspectives for buyers, sellers, and intermediaries navigating the “Main Street” M&A market.

Many of our articles are written by freelance writers. We are always looking for new talent. If you're a great writer who writes about business, real estate, investing, or finance, we'd like to talk to you. Send us an email at submissions@dealstream.com.