Understanding Revenue-Based and Invoice-Based Financing

Alternative Sources of Business Funding

Startups and small businesses often face challenges in securing traditional bank loans. Limited credit histories, inability to meet collateral requirements, or being deemed “high risk” often push these businesses to seek alternative financing solutions. Fortunately, options such as revenue-based financing and invoice-based financing may provide viable alternatives.

Revenue-Based Financing: A Flexible Solution

Revenue-based financing, also called royalty-based financing, enables businesses to secure capital without giving up equity or pledging collateral. Instead, businesses receive funding based on a percentage of their future revenue, offering a dynamic repayment structure that adjusts with the company’s cash flow. This model can be particularly beneficial for startups and small businesses that may struggle to qualify for traditional loans.

How Revenue-Based Financing Works

The process of obtaining revenue-based financing typically includes the following steps:

- Application: Businesses apply for funding, providing financial and operational details.

- Assessment: Lenders evaluate the business’s growth potential and revenue stability to determine the loan terms.

- Funding: Approved businesses receive an upfront lump sum.

- Repayment: Repayments are tied to a percentage of monthly revenue, ensuring flexibility during slower periods.

Benefits of Revenue-Based Financing

- No collateral required: Businesses can access funds without risking their assets.

- Flexible repayment terms: Payments scale with revenue, making it easier to manage cash flow.

- Accessibility: Startups and businesses with limited credit history can qualify.

- Growth-oriented: Funds can be used for expansion, marketing, or other growth initiatives.

Drawbacks of Revenue-Based Financing

- Higher costs: Interest rates tend to be higher than traditional loans.

- Restrictive Decision-Making: The lending agreement may have clauses which impact business decision-making.

Invoice-Based Financing: Unlocking Cash Flow

Invoice-based financing, referred to as invoice financing or invoice factoring, help businesses convert unpaid invoices into immediate cash. While the terms invoice financing and invoice factoring are often used interchangeably, they involve distinct processes.

Invoice Financing

Invoice financing allows businesses to borrow against their unpaid invoices while retaining control over collections. Lenders advance a percentage of the invoice value and charge fees or interest on the borrowed amount.

Invoice Factoring

Invoice factoring, on the other hand, involves selling unpaid invoices to a factoring company at a discount. The factoring company assumes responsibility for collecting payments from customers.

How These Options Work

- Application: Submit unpaid invoices to the lender or factoring company.

- Assessment: The creditworthiness of the customers is reviewed.

- Funding: A percentage (usually 70-85%) of the invoice value is advanced.

- Collection: For factoring, the company collects directly from customers; for financing, the business collects payments and repays the loan.

- Settlement: The remaining balance is paid to the business, minus fees or discounts.

Benefits of Invoice Financing and Invoice Factoring

- Immediate cash access: Businesses can unlock funds within days.

- No equity dilution: Owners retain full control of their business.

- Improved cash flow: Helps cover payroll, supplier payments, or operational expenses.

- Industry suitability: Ideal for industries with long payment terms or seasonal fluctuations.

Drawbacks of Invoice Financing and Invoice Factoring

- Factoring fees: These reduce the overall funds received.

- Limited availability: Companies with weak financials or risky invoices may not qualify.

- Client relationships: Factoring may affect client perceptions, as customers interact directly with the factoring company.

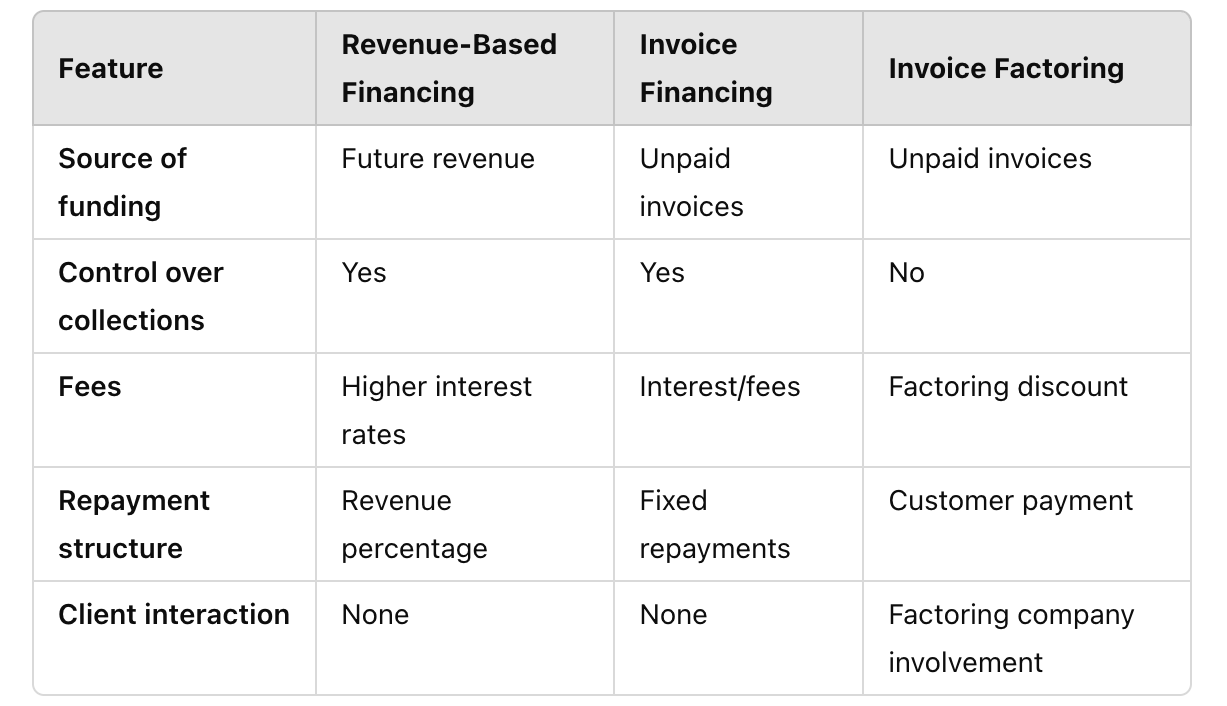

Comparing Revenue-Based Financing, Invoice Financing, and Invoice Factoring

While revenue-based financing focuses on future revenue, invoice financing and factoring leverage existing invoices to provide funding. Here's a comparison:

Alternatives to Revenue-Based Financing

Although revenue-based financing offers unique benefits, it's essential to consider other financing options to determine the best fit for your business before you make a decision. Some alternatives include:

- Business loans: Traditional bank loans can provide fixed interest rates and longer repayment terms. They often require collateral and a strong credit history, however, which can make them more of a challenge to get for new businesses.

- Lines of credit: A line of credit offers flexible access to funds as needed, which is a great fit for some businesses, especially as they incur rolling expenses. However, it may have higher interest rates than a fixed-term loan. With a line of credit, you can pull from funds as you need them, only paying interest on your current draw.

- Merchant cash advances: This option involves receiving a lump sum upfront in exchange for a percentage of future sales. Do note it can be expensive due to high-interest rates and fees. Many of these loans come with daily interest payments, which can place a high burden on your ability to maintain cash flow while also repaying what you’ve borrowed.

- Crowdfunding: Platforms like Kickstarter and Indiegogo allow businesses to raise funds from a large number of individuals. But it’s important to remember crowdfunding can be time-consuming and may not guarantee success.

- Government-backed loans: The Small Business Administration (SBA) and other government agencies offer loans with favorable terms for small businesses, including high capital amounts, low interest rates, and long repayment timelines. SBA loans are highly competitive, though, and often require a track record in business for approval.

Choosing the Right Option

When deciding on a financing solution, evaluate your business’s specific needs, cash flow dynamics, and growth goals. Consider:

- Cash flow predictability: Revenue-based financing suits businesses with consistent revenue, while invoice financing/factoring works for those needing to address cash flow gaps.

- Cost considerations: Weigh fees, interest rates, and repayment flexibility.

- Customer relationships: Factoring may impact how clients view your business.

The Bottom Line on Revenue-Based Financing and Invoice Financing

Revenue-based financing and invoice financing offer unique advantages and disadvantages for businesses seeking capital. Revenue-based financing provides flexible funding without collateral but can involve higher interest rates. Invoice financing offers quick access to cash but may have limited availability and involve factoring fees. By carefully considering your business's specific needs, financial health, and industry-specific factors, you can confidently select the financing option that best aligns with your goals and supports your growth.

Many of our articles are written by freelance writers. We are always looking for new talent. If you're a great writer who writes about business, real estate, investing, or finance, we'd like to talk to you. Send us an email at submissions@dealstream.com.